State and local tax policy plays a critical role in shaping corporate site location decisions. The level and structure of taxes imposed by state and local governments directly influence where companies choose to invest, expand, and create jobs. While these taxes fund essential public services such as schools, infrastructure, water systems, and public safety, they also function as a policy lever that can either attract or discourage corporate investment.

According to the Council of State & Local Taxes (COST) 2024 annual report, businesses paid $1,096.2 billion in state and local taxes in FY23, accounting for 44.7 percent of all state and local tax revenue. Of that total, $595.7 billion was paid in state taxes, representing a 0.9 percent increase from the prior year, while $500.4 billion was paid in local taxes, a 7.3 percent increase. Combined, business tax payments grew 3.7 percent year over year, underscoring the growing importance of state and local tax policy in corporate decision-making.

Source: Council of State Taxation

Property taxes remain the largest business tax burden in nearly every state, and most states also impose some form of income tax. When evaluating state and local tax policy, companies must assess which taxes will most directly impact their operations. Large-scale industrial investments often face significant property tax exposure, particularly in states that tax manufacturing equipment or inventory. By contrast, companies in advanced services, white-collar, or technology sectors may place less emphasis on property taxes due to smaller physical footprints and increased reliance on virtual or flexible office environments.

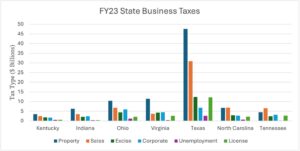

Comparing state and local tax policy across Indiana, Kentucky, North Carolina, Ohio, Texas, and Virginia illustrates how tax structures affect industries differently. In Kentucky, Indiana, and Ohio, property taxes represent the dominant tax burden for many businesses, while income taxes help spread revenue collection to individual taxpayers. States without an income tax, such as Texas, shift a greater share of the tax burden to businesses through higher sales and property taxes. Meanwhile, states like Tennessee and North Carolina, which have economies and population sizes comparable to Ohio, have adopted state and local tax policy frameworks that place a lower overall burden on businesses by relying more heavily on sales taxes that are generally more favorable to manufacturing and office projects.

Source: Council of State Taxation

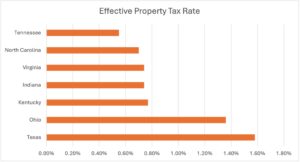

Property taxes have an especially significant impact on commercial development. As data from the Council on State Taxation shows, taxes on real and personal property are the largest source of state and local tax revenue. Compounding the challenge for companies, property tax rates are rising nationwide and have doubled in some markets. High property taxes can discourage large capital investments and job creation, particularly when property values are reassessed upward following new development.

Source: Council of State Taxation

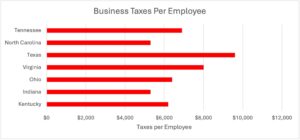

Evaluating state and local tax policy on a per-employee basis provides additional insight into a state’s overall business climate. This approach accounts for population differences and offers a clearer comparison of tax burden across states. Data shows that Texas, Virginia, Ohio, and Kentucky impose some of the highest per-employee state and local tax burdens, while Indiana and North Carolina maintain comparatively lower levels. Indiana consistently ranks as a leader in maintaining a low tax burden for local businesses.

Source: Rocket Mortgage

Tennessee stands out for keeping property tax rates relatively low, while Texas relies heavily on property taxes due to the absence of an income tax. Ohio presents a more complex challenge, as high effective property tax rates persist despite the presence of income and sales taxes at multiple levels of government. In response to growing concern over property tax burdens and a proposed constitutional amendment to eliminate the tax entirely, the Ohio General Assembly has recently enacted measures aimed at providing property tax relief.

Ultimately, state and local tax policy can create either a competitive advantage or a disadvantage for companies evaluating where to locate high-wage jobs and capital investments. States and communities that align tax policy with economic development goals are better positioned to compete for corporate site location projects in an increasingly competitive national and global marketplace.