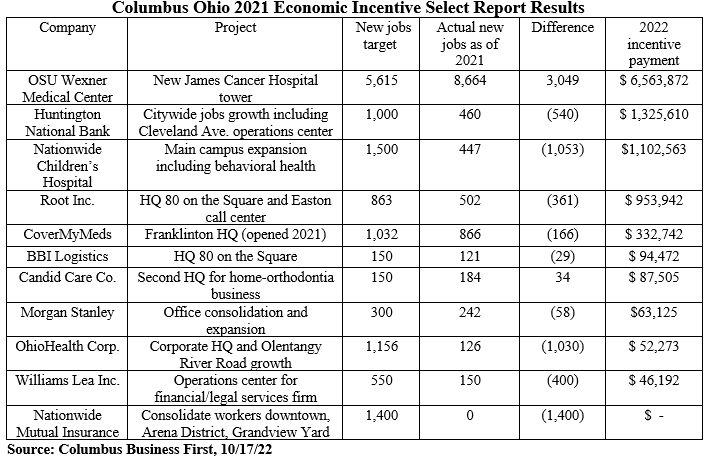

An economic downturn coming in 2023 driven by rising interest rates and rising costs will increase the importance of compliance with existing economic development incentive agreements—creating a critical 2023 corporate site location trend. As the table below from Columbus, Ohio-based economic development incentive reports, Work from Home (WFH) also has had a major impact on the company’s ability to gain the benefits promised by economic development incentive agreements.

McKinsey estimates that at least $90 B in state and local government economic development incentives are used by companies to spur corporate site location growth in the United States. That money is not free. Economic development incentive awards all come with some form of agreement, and many are “performance-based incentives” that trigger a financial reward for a company when they report the achievement of high-wage job creation and capital investment. In short, the backside of economic development incentives is the reporting requirements and compliance measures needed to gain the company’s benefit.

Ohio offers a model for economic development incentive compliance at the local and state government level. Ohio, like all state economic development programs, requires substantial compliance requirements. As an example, annual reporting requirements compliance exists tied to the Ohio Job Creation Tax Credit as well as the state of Ohio’s two property tax abatement programs- Community Reinvestment Area (CRA) and Enterprise Zone (EZ) programs. These program’s annual reports are due in March and the Montrose Group would be glad to discuss how our firm can assist your company or community to make meet state economic development incentive requirements through these annual reports.

The Ohio Job Creation Tax Credit Program requires taxpayers to annually submit to Development a report detailing information pertaining to the taxpayer’s project. Complete annual reports must be submitted by March 1 each year. The Ohio Department of Development requires annual progress reports to be filed for the year in which the tax credit begins and consecutive years throughout the term of the tax credit. The annual progress report is filed online using the link in the dropdown menu on the left. Information requested in the annual progress report includes the number of full-time equivalent employees for the project; total payroll for the project; Ohio employee payroll for the project; income tax revenue for the project; the amount of relocated payroll for the project during the tax year; and other information Development deems appropriate Taxpayers who fail to submit a complete annual report by the deadline shall be assessed a $500 late fee for each ensuing calendar month until the report is filed and may be subject to other remedies. Upon verification of information submitted in the annual progress report, a tax credit certificate is issued to the taxpayer.

The 2022 EZ Annual Report includes two separate reporting requirements:

- Zone Report to catalog the aggregate activity in the EZ. This report must be completed every year, even for Enterprise Zones with no active exemptions; and

- Company Reports for active exemption agreements. If an EZ does not have any active commercial or industrial exemption agreements, completion of a Company Report is not required.

Each EZ created prior to January 1, 2023 and certified by Development must complete and submit an annual report form that covers all exemptions in the EZ through December 31, 2022. Completing the EZ annual report is done on an online portal to the Ohio Department of Development. No paper or emailed copies of the Zone Report or Company Reports will be accepted. EZ Managers are encouraged to retain signed copies of the completed worksheets they receive back from business owners that are recipients of EZ agreements, but submission to the Ohio Department of Development is only to be done through the EZ Annual Reporting Module as noted above. Company Reports should be filed before you complete the Zone Report. This is due to the Zone Report requiring aggregated information from all the Company Reports, and the 2022 EZ Annual Report must be filed with Development by March 31, 2023.

CRA annual reports of course differ if they are a Pre-1994 CRA compared to a Post-1994 CRA. Pre-1994 CRAs were created before 1994 and they offer a 100%, 15-year real property tax abatement if a company creates jobs located in a valid Pre-1994 CRA. Pursuant to Ohio Revised Code (ORC) Section 3735.69(B), any municipal corporation or county that has created a CRA prior to July 1, 1994, is required to submit to Development an annual status report summarizing the activities and projects that have been granted a real property tax exemption within the CRA. This report is to address active CRA exemptions during 2021 including projects certified by the Housing Officer to the County Auditor through December 31, 2021. Communities must complete one report form for each Pre–1994 CRA in their jurisdiction. Please note that pursuant to ORC Section 3635.672, CRAs created after July 1, 1994, and Pre-1994 CRAs invoking the new rules are required to be confirmed by Development and receive a more extensive reporting format. In completing the 2021 Pre-1994 CRA Annual Report, the Ohio Department of Development asks the communities to provide the best available information for the period ending December 31, 2021. In many instances, the property owner or tenants may need to be contacted to verify information, including job creation figures. The 2021 Pre-1994 CRA Annual Report should be submitted to Development by March 31, 2022.

The 2022 CRA Annual Report (for Post 1994 CRAs) includes three separate required reporting requirements:

- An Area Report to catalog the aggregate activity in the CRA- this report needs to be completed every year, even for CRAs with no active exemptions.

- Company Report for active commercial or industrial exemption agreements, (if the CRA has active commercial/industrial exemptions); and

- Residential Status Report for residential incentives if the CRA offers residential incentives and has at least one active residential exemption.

Each CRA created prior to January 1, 2023 and confirmed by the Ohio Department of Development (Development), must complete and submit an annual report form that covers all exemptions in the CRA through December 31, 2022. Entries for the report include local incentives annual report entry; login/password; electronic filing with retention of paper copies recommended; company reports to be filed before the area report is; and residential status reports to be included as well. The 2022 CRA Annual Report must be filed with the Ohio Department of Development by March 31, 2023.

Compliance with economic development incentives is another opportunity for a company and a community to negotiate the impact of changing market conditions beyond merely reporting results. Economic development incentive agreements should include flexibility for local and state governments to implement the incentive in case the company does not meet the promised job and capital investment commitments. This flexibility can include gaining less of the promised economic development incentive or even the termination of the agreement. In some cases, local and state governments may have the authority to claw back previously awarded incentives. Failure by the company to meet its promised job creation and capital investment goals is not a simple matter and professional representation from the Montrose Group or others is a smart move.

Many economic development agreements contain “Market Conditions and Other

Factors” provision that gives the government or economic development organization partner the ability to keep the incentive agreement in place if the company does not meet its economic development commitments due to factors outside of their control. “Market Condition” clauses have their roots in the common law legal concept known as Force Majeure. Force Majeure gives the ability of parties to a contract to be excused from their obligations when certain circumstances arise beyond the party’s control making performance inadvisable, commercially impracticable, illegal, or impossible. Force Majeure is triggered through a contract provision that list extreme events such as epidemics or pandemics, along with war, terrorist attacks, “acts of God,” famine, strikes, and fire in the list of events excusing overall performance or delay in performance.

Economic development incentive agreements may give the local and state economic development officials the ability to relieve the company impacted by dramatic events outside of their control from job creation and capital investment commitments. This flexibility is critical as many economic development incentive agreements permit local and state governments to “claw back” tax incentives previously awarded or terminate the tax incentive agreement even though the company may well pick up economic production following the dramatic event. Local and state government officials deciding whether to avoid tax incentive penalties for a company under a Market Condition or Force Majeure clause may ask a couple of key questions:

⦁ Does the company believe it will survive the event and recover following the event?

⦁ Is there another company in place to implement these economic commitments?

⦁ What is the company impact of any federal, state, or local regulatory requirements?

Communication is the key to successfully utilizing a Market Condition or Force Majeure clause in an economic development agreement. Corporate site location consultants or competent legal counsel can help negotiate good results for clients with local and state economic development leaders who are focused on helping the company succeed.

State and local economic development programs require companies and communities to comply with reporting requirements to gain tax benefits but also to comply with incentive agreements.

Contact Dave Robinson at [email protected] if the Montrose Group can assist with any economic development incentive compliance reports.