A data center is a physical facility that organizations use to house their critical computer applications and data. Several types of data centers operate including enterprise data centers that a single company houses on corporate campus; managed services data centers run by third party providers; colocation data centers where a company rents space within another’s data center; and cloud data centers where off-premises data and applications are hosted by a cloud services provider such as Amazon Web Services (AWS), Microsoft (Azure), or IBM Cloud or others. Data center capex will grow at a 6% CAGR to reach just over $200 B over the next five years.

Data centers are primarily located in or near major urban centers across the United States. CBRE reports that the U.S. wholesale data center primary markets—Atlanta, Chicago, Dallas/Ft. Worth, New York Tri-State, Northern Virginia, Phoenix and Silicon Valley—accounted for more than 56% of the record annual absorption in 2018 with 60% of construction of data centers in 2019 at one point in Northern Virginia.[i] However, the exponential growth of data requirements in the country has been fueling data center construction, but a data center cost index 2019 study suggested that in the United States, Dallas, North Virginia, and Phoenix were the “overheated” markets for Data Center construction in 2019. JLL further reports data center demand remains robust in the first half of 2020, with eight out of the 14 markets in the United States showing a year-over-year increase.[ii] Last year, these same domestic markets absorbed 171.2 MW, compared to 288.2 MW in H1 2020.[iii] Total absorption reached 295.2 MW in the United States, including Salt Lake City’s 7.0 MW figure, but, again, Northern Virginia leads the way in demand, as absorption increased from 76.1 MW in H1 2019 to 180.0 MW in H1 2020.[iv] New Jersey and Northern California increased absorption by 11.8 MW and 10.2 MW, respectively, year-over-year.[v]

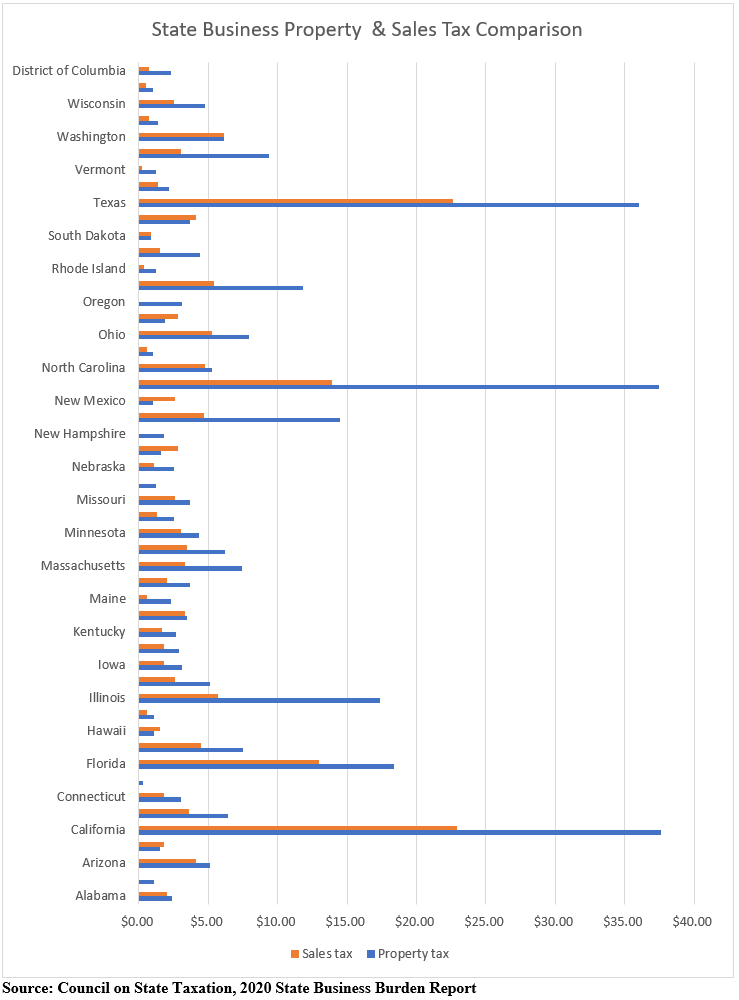

Few industries are as sensitive to tax policy and incentives as data centers. Other than needing a small number of highly skilled high-tech workers, these facilities need a location safe from natural disaster, with reliable and affordable electric rates and water, and a competitive tax structure. Data centers pay substantial sales and property taxes. There are 11 states that automatically do not assess property taxes on equipment and furniture. These states include Delaware, Illinois, Iowa, Kansas, Minnesota, New Jersey, New York, North Dakota, Ohio, Pennsylvania, and South Dakota, and 19 states offer some form of property tax abatements data centers can attempt to gain through a corporate site location process.[vi] Sales tax is another substantial cost center for both the operation and construction of data centers, and many states offer aggressive economic development incentives to address their high sales tax costs which often provide revenue for local and state governments. As the table below illustrates, traditional high-cost states like California, New York and Illinois have substantial sales and property taxes in place as well as every other tax government can think of. Texas and Florida’s very high sales and property tax illustrates the downside of not having a state or local income tax. This business sales and property tax burden illustrates the needed for data center economic development incentives.

As most data centers are not “worker heavy” traditional state data center tax incentives generally are not focused on the job creation tax credits used for other industries but instead address sales and property taxes, construction, and electricity costs. The list below outlines the existing state data center tax incentive programs.

| Alabama data processing center projects are eligible for a tax abatement of all state and local non-educational sales and use taxes associated with constructing and equipping a project for an extended time period contingent upon the total capital investment in the project. For these projects, the maximum abatement period is: 10 years for projects that invest up to $200M within 10 years from the commencement of the project; 20 years for projects that invest over $200M but less than $400M within 10 years from the commencement of the project; 30 years for projects that invest over $200M within 10 years from the commencement of the project and exceed $400M within 20 years from the commencement of the project.[i] |

| Arizona offers data centers an exemption from the Transaction Privilege Tax and Use Tax exemptions at the state, county, and local levels, on qualifying data center purchases for an owner, operator or qualified co-location tenant of a data center who may receive the exemptions provided by the incentive for up to ten full calendar years following the year certification of the data center is issued. If the data center qualifies as a Sustainable Redevelopment Project, the exemptions are available for up to 20 full calendar years following the year certification of the data center is issued. If the data center is located in either Maricopa or Pima County, a Capital Investment of at least $50 million is made within five years of the date of the Letter of data center Certification from the Arizona Commerce Authority, if the data center is located in any county other than Maricopa or Pima, a capital investment of at least $25 million is made within five years of the date of the Letter of data center certification from the Arizona Commerce Authority; or, in the case of an existing data center, regardless of location, a capital investment of at least $250 million was made during the period between September 1, 2007 and August 31, 2013.[ii] |

| Arkansas does not offer a data center specific tax incentive but data centers meeting job creation and capital investment requirements may negotiate sales and use tax exemptions and rebates, tax credits and closing fund contributions.[iii] |

| Georgia offers two possible ways for data centers to qualify for sales and use tax exemptions on qualifying purchases: New (signed into law May 2018): Co-located data centers and single-user data centers that invest $100 million to $250 million in a new facility may qualify for a full sales and use tax exemption on eligible expenses, which include equipment under current data center exemption and computers, emergency backup generators, air handling units, cooling towers, energy storage or energy efficiency technology and many other items and the minimum required investment in the new facility is tied to the population of the county in which the data center locates; and Georgia also has a full sales and use tax exemption on certain computer equipment purchased by high-tech companies that invest a minimum of $15 million in qualifying equipment. To be eligible, the company must be classified under certain relevant NAICS codes, which include single-user data centers (but not co-located data centers), software publishers, computer systems design, certain telecommunications firms, financial transaction processing facilities and R&D centers.[iv] |

| Idaho offers new data centers a potential sales tax exemption on server equipment as well as construction materials used in the construction of the data center facility for companies that create and maintain at least 30 new jobs in Idaho within the first two years after beginning operations, paying an average wage that is at or above the county average for the county in which the data center is located and make a capital investment of at least $250,000,000 within 5 years after construction begins and be solely devoted to the purpose of providing the data center, or have a separately operated segment of a business solely devoted to the purpose of providing the data center.[v] |

| Illinois’ data centers investment program provides data center owners and operators with a tax credit of 20% of wages paid for construction workers for projects located in underserved areas with new and existing data centers and their tenants collectively making a capital investment of at least $250 million over a 60-month period for a term of 20 years, the data center owner/operator and its tenants create at least twenty (20) full-time or full-time equivalent new jobs associated with the operation or maintenance of the data center, total compensation for these jobs must be equal or exceed 120% of the median wage paid to full-time employees in the county where the data center is located, the data center must also be carbon neutral or attain certification under one or more green building standards and located in an underserved area.[vi] |

| Indiana Data Center Gross Retail and Use Tax Exemption provides a sales and use tax exemption on purchases of qualifying data center equipment and energy to operators of a qualified data center for a period not to exceed 25 years for data center investments of less than $750 million. If the investment exceeds $750 million, the IEDC may award an exemption for up to 50 years. Indiana local governments may also provide a personal property tax exemption on qualified enterprise information technology equipment to owners of a data center who invest at least $25 million in real and personal property in the facility.[vii] |

| Iowa data centers may be eligible for 50 or 100 percent refund on sales and use tax for: electricity purchased for use in data centers; power infrastructure equipment; computer purchases; temperature control equipment; cool tower equipment; racking systems, including cabling.[viii] |

| Kentucky offers a sales tax refund for computer equipment for data centers investing $100 M.[ix] |

| Florida offers a data center property tax exemption for a data center’s owners and tenants with a $150 million capital investment, critical IT load of 15 megawatts and a critical IT load of 1 megawatt or higher dedicated to each individual owner or tenant within the data center met within 5 years of construction.[x] |

| Michigan offers data centers a potential sales tax exemption for data center equipment at qualified data centers and for qualified data centers operating in designated renaissance zones may gain both real and personal property tax exemptions.[xi] |

| Maryland data centers that for a 10-year consecutive benefit period create five jobs over three years paying 150% of state minimum wage and make a minimum investment of at least $2 million in qualified data center personal property for a business located within a Tier 1 Area, and at least $5 million in qualified data center personal property for a business located in any other area of the State, and the benefit period expands to 20 years, subject to annual renewal, if the business invests at least $250 million in qualified data center personal property within the first ten years after submitting an application.[xii] |

| Minnesota companies that build data or network operation centers of at least 25,000 square feet and invest at least $30 million within 48 months may qualify for a sales tax exemptions for up to 20 years on: computers and servers; cooling and energy equipment; energy use; software; and pay no personal property tax, and Minnesota does not tax: personal property, inventories, utilities, internet access, information services, and custom-c reated software, and companies that substantially refurbish a data or network operations center of at least 25,000 square feet and invest at least $50 million within 24 months may qualify for the Data Center Sales Tax incentives.[xiii] |

| Mississippi provides data centers with a sale and use tax exemption for all new and replacement computing equipment and software. Data centers must invest at least $20 million and must create at least 20 new jobs paying 125 percent of the average state wage to qualify for this program.[xiv] |

| Missouri offers a data center company or a consortium of eligible companies who plan to locate at a new or existing data center facility with at least 5 new full time jobs with average wages at 150% of county average wage within 24 months and $5 million dollars in new investment within 12 months of the project approval, or at least 10 new full time jobs with average wages at or above 150% of county average wage and $25 million dollars in new investment within 36 months of the project approval, for an existing facility, an exemption on state and local sales and use taxes used for expanding operations for a specified maximum amount for each year for 10 years or, for new facilities an exemption of 100% of the state and local sales and use taxes for a specified maximum amount for each year for 15 years applied to construction or rehab materials; machinery and equipment purchases; and utility costs over a designated term at the facility, and projects may be eligible for a local government property tax abatement through the Chapter 100 Bond program.[xv] |

| Montana offers Qualified Data Centers with at least 25,000 square feet of new or expanded area, where the total cost of land, improvements, personal property, and software is at least $50 million invested during a 48-month period with construction commencing after January 1, 2019 a property tax abatement of 75% or 50% of their taxable value in the first five years after a construction permit is issued, with each year thereafter, the percentage must increase by equal percentages until the full taxable value is attained in the tenth year, approved by the corresponding county jurisdiction. |

| Nebraska offers Tier 2 data centers valued at $200 million in new investment and 30 new full-time jobs a full refund of the sales tax paid for qualified capital purchases at the project, the full sliding scale wage credit of 3%, 4%, 5%, or 6% depending on wage level, and a 10% investment tax credit.[xvi] |

| Nevada offers a sales and use tax abatement reducing the rate to 2% for 10 or 20 years and requires the Governor’s Office of Economic Development Board to approve a reduction to 2% by a two-thirds vote, and if this is not approved, the abatement will be reduced to 4.6%, and a 10 year and a 20 year tax abatement program: 10 year abatements: requires within 5 years creation of 10 jobs for Nevada residents paying 100% of the statewide average wage making $25 million in capital expenditures; and 20 year abatements: requires within 5 years creation of 50 jobs for Nevada residents paying 100% of the statewide average wage making $100 million capital expenditures. Co-located tenants must enter into a minimum two-year agreement with the applicant to use or occupy space at the data center and obtain a business license issued by the Secretary of State; and data centers must maintain the business in Nevada for 10 years, register pursuant to the laws of Nevada, offer medical insurance plan, and pay at least 65% of the plan’s premium costs, and ensure that 50% or more of all workers engaged in construction of the data center are Nevada residents.[xvii] |

| New York for an Internet data center operator who operates a data center specifically designed and constructed as a high security environment for the location of servers and similar equipment that hosts Internet Web sites; and provides uninterrupted Internet access to customers’ Web pages exempts the payment of sales tax on the purchase or use of machinery, equipment, and certain other tangible personal property that includes: computer system hardware, such as servers and routers; pre-written computer software; storage racks and cages for computer equipment; property necessary to maintain the appropriate climate-controlled environment, such as air-filtration equipment, air-conditioning equipment, and vapor barriers; power generators and power conditioners; property that will constitute raised flooring when installed; and other similar equipment, as well as building systems that are designed for an Internet data center, such as interior fiber optic and copper cables; fire control, such as fire suppression equipment and alarms; and maintaining a secure environment, such as protective barriers if the exempt property is placed or installed in the Internet data center for use there; and required for and directly related to providing Internet Web site services for sale, and Internet data center operators may purchase the following services exempt from tax when the services are provided directly to or in relation to exempt Internet data center property: installing, maintaining, servicing, and repairing qualified tangible personal property; maintaining, servicing, and repairing qualified real property; and protective and detective services.[xviii] |

| North Carolina provides three sales and use tax exemptions for purchase of electricity and support equipment providing service or function included in the business of an owner, user or tenant of the data center, the generation, transformation, transmission, distribution or management of electricity, including exterior substations, generators, transformers, unit substations, uninterruptible power supply systems, batteries, power distribution units, remote power panels and other capital equipment for these purposes; HVAC and mechanical systems, including chillers, cooling towers, air handlers, pumps and other capital equipment used for these purposes; and hardware and software for distributed and mainframe computers and servers, data storage devices, network connectivity equipment and peripheral components and equipment, or providing related computer engineering or computer science research purchased for a “Qualifying Data Center investing $75 M within 5 years paying the county wage standard and providing health insurance, certain business property purchased for an “Eligible Internet Data Center” in Tier 1or 2 North Carolina counties for projects investing $250M within 5 years focused on software publishing; and computer software, defined as a set of coded instructions designed to cause a computer or automatic data-processing equipment to perform a task, at a “Data Center” that is defined as a facility that provides infrastructure for hosting or data-processing services and is concurrently maintainable, the power and cooling systems serving the computer equipment must include redundant capacity components and multiple distribution paths, and, although the facility must have multiple distribution paths serving the computer equipment, a single distribution path may serve the computer equipment at any one time.[xix] |

| Ohio provides a sales-tax exemption on the purchase of eligible data center equipment including equipment cooling systems to manage the performance of computer data center equipment, to generate, transform, transmit, distribute, or manage electricity necessary to operate the tangible personal property used or to be used in conducting a computer data center business, and building and construction materials sold to construction contractors for incorporation into a computer data center with $100M investment and $1.5M in payroll, and data centers are eligible for property tax abatements negotiated at the local gover nment level.[xx] |

| North Dakota owners, operators, and tenants of a qualified, 16,000 square foot data center may be granted a sales tax exemption on information technology equipment and computer software, including replacement equipment and software, purchased between January 1, 2015, and December 31, 2020. The exemption is limited to the first four qualified data centers approved by the Tax Commissioner and 4 data centers have been awarded the incentive. To qualify, a data center must be a newly constructed or substantially refurbished facility of at least sixteen thousand square feet located in North Dakota.[xxi] |

| Oklahoma computer services and data processing facilities in NAICS codes Numbers 5112 and 5415 may be eligible for a 5 year exemption from Ad Valorem Tax if they derive at least 50% of their annual gross revenues from the sale of a product or service to an out of state customer or buyer, invest $250,000 or more in construction, acquisition or expansion cost of the manufacturing facility and; have a net increase in annualized payroll of at least $250,000 if the facility is located in a county with a population of fewer than 75,000, or at least $ 1 million dollars if the facility is located in a county with a population of 75,000 or more in the initial application year. Establishments in NAICS codes 5142 must meet the following qualifications: 80% of annual gross revenues from the sale of a product or service to an out of state customer or buyer; invest $7 million dollars or more in capital improvements and; have a net increase in annualized payroll of at least $250,000 if the facility is located in a county with a population of fewer than 75,000, or at least $1 million dollars if the facility is located in a county with a population of 75,000 or more in the initial application year. [xxii] |

| Oregon data centers may gain an enterprise zone property tax abatement on the new plant and equipment for 3-5 years in rural communities.[xxiii] |

| Pennsylvania provides up to a $5M tax refund on sales and use taxes for data center equipment.[xxiv] |

| South Carolina may exempt from some sales and use taxes when a data center is expanding and/ or new facility is certified by the South Carolina Department of Commerce as a qualifying datacenter and invests at least $50 million (or a combined $75 million with one or more other companies) in real or personal property at a single facility over a five-year period, create at least 25 new jobs within a five-year period with an average wage that is at least 150% of the state or county per capita wage, whichever is lower, and maintain the 25 jobs for at least three years. The items that may be exempt from sales and use tax are computer equipment, software and electricity directly used in datacenter operations, and once qualified for this exemption, all future computer equipment purchases are exempt.[xxv] |

| Tennessee offers data centers a sales tax exemption for certain hardware and software purchased for a qualified data center with a minimum capital investment of $100M and 15 new full-time positions paying at least 150% of the state’s avg. occupational wage; investment must be made during a 3 yr. period but can be extended to 5 yrs. for investments under $1B or 7 yrs. for investments exceeding $1B with the state’s permission.[xxvi] |

| Texas offers data centers with 100,000 sq. ft. creating 20 and $200M in capital investment over a 5-year period that are constructed or refurbished for use primarily as a facility to house servers and related equipment and support staff in the processing, storage and distribution of data, have, or will have, an uninterruptible power source, generator backup power, a sophisticated fire suppression and prevention system, and enhanced physical security that includes restricted access, video surveillance and electronic systems, not be used primarily by a telecommunications provider to deliver telecommunications services; and not be subject to an agreement limiting the appraised value of the data center’s property can qualify for a 100% exemption on sales and use tax.[xxvii] |

| Virginia offers data centers equipment sales tax exemption for projects with $150M investment creating 50 jobs paying 150% of average wage or 25 jobs in underserved markets in Virginia Enterprise Zones and permits end users at the data centers to gain access to the incentive.[xxviii] |

| Washington offers data centers a retail-sales and use tax exemption for purchases and labor installation costs for eligible server equipment and power infrastructure.[xxix] |

| West Virginia values tangible personal property, including servers, directly used in a high-technology business or in an Internet advertising business, for property tax purposes at 5% of the original cost of the property, and eliminates the sales tax from all purchases of prewritten computer software, computers, computer hardware, servers, building materials and tangible personal property for direct use in a high-technology business or internet advertising business.[xxx] |

| Wyoming offers several data center incentives including a $2.25M max grant for Managed Data Center Cost Reduction Grant Program Is a $2.25 Million to reimburse accrued utility expenses for power or broadband over 3 years and for each grant the business must create a match of at least 125% of the grant amount in payroll and capital expenditure with the caveat that 50% of the match will be in payroll creation, and have a payroll must be greater than 150% of the county’s median wage, a Data Center Permit Exemption for a mega-data center project which exceeds $178.3 Million in capital investment, would be exempt from the requirement of applying for an Industrial Siting Permit through the Wyoming Department of Environmental Quality providing a cost savings of approximately $500,000 associated with permit application preparation, wildlife studies, economic analyses, public meetings, permit hearings, attorney fees, etc., a Data Center Sales Tax Exemption that requires a $5 Million investment in capital infrastructure (building, walls, engineering, dirt work, etc.) in a Wyoming location in addition to a $2 Million or larger investment in data center equipment (servers, peripheral equipment and data center containers) and software purchases, and the Wyoming Legislature approved a $15,000,000 appropriation to assist Wyoming cities, towns and counties to build necessary public infrastructure for the recruitment and operation of data centers.[xxxi] |

Data centers will continue to be a hot item in 2021 and prime locations and solid tax policy are the keys to recruiting them.

[i] https://www.cbre.com/research-and-reports/2020-US-Real-Estate-Market-OutlookDataCenters#:~:text=New%20deliveries%20will%20increase%20the,between%20certain%20markets%20in%202020.&text=Adding%20momentum%20headed%20into%202020,IT%20and%20real%20estate%20decisions.

[ii] https://www.us.jll.com/content/dam/jll-com/documents/pdf/research/data-center-outlook-h1-2020.pdf

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] https://f.tlcollect.com/fr2/813/17870/Impact_of_Taxes_and_Incentives_on_Data_Center_Locations_(2013).pdf