Housing is joining workforce development to become a major corporate site location trend in 2023. Growing regions like Central Ohio are developing 2.5 jobs for every 1 residential permit creating a housing shortage. Regions not growing are failing to develop substantial residential growth. Finally, rural regions are losing population at an alarming rate and desperately need new residential products to retain existing employers and to keep their young people. No matter where you are in the United States, the availability of attainable housing that young and old alike can afford is needed. The simple fact is regions cannot retain and attract companies without workers—workers won’t go to regions where they cannot afford housing.

Economic development organizations and communities have become accustomed to the traditional corporate site location process that positions sites for investment opportunities. EDOs have spent decades working to build and market an inventory of shovel-ready sites, equipped with water, sewer, electric, gas, broadband, and roads at the “front door” to those sites; communities have established incentives districts to demonstrate their commitment to having skin in the game to win projects, and site selection firms have developed advanced location analytics tools to find ideal geographic locations for clients. While these approaches to finding the ideal location play an important role in attracting companies, there is a shifting tide in the corporate site location process. Communities must look beyond traditional incentive programs and think about the new incentive – successfully attracting residents and the workforce.

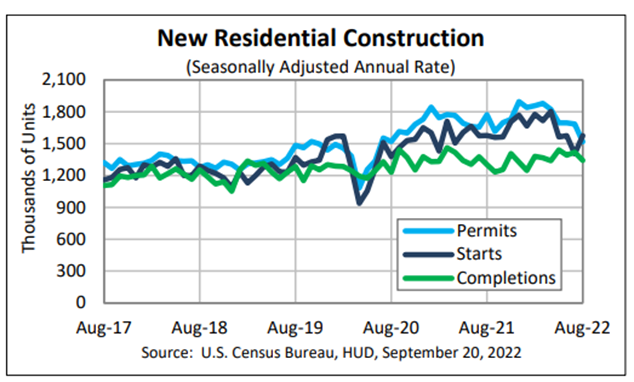

Record-high job openings, turnover, low unemployment, and local governments opposed to additional housing development have sent companies scrambling to find creative attraction and retention strategies, and housing has become one of them. Despite an uptick in new residential permits issued since August 2017, new housing completions are significantly lagging and creating a growing gap in the number of single-family homes coming online. Supply chain disruptions and price hikes incurred during the COVID-19 pandemic have not helped the national demand for housing stock, pushing companies to look for creative ways to bring new inventory online and close the labor demand gap.

Booming regions such as Columbus, Ohio are facing a crisis not driven by high-wage job creation but the lack of available housing. Supported by the global corporate site location win of gaining a $20 B Intel “fab” manufacturing plant, Columbus is expected to add over 50,000 jobs in the coming decade. The simple fact is Columbus has not been keeping up with their growth from a housing standpoint for decades. Housing experts estimate that one new housing permit is needed for every new, net job created. Thus, housing needs to be developed on a one-to-one ratio. According to a recent VSI study, the Columbus region has been developing 95 housing permits for every 100 net, new jobs created. More importantly, all income levels will need housing in the Central Ohio marketplace. From the rich to the poor, the availability of housing is a critical corporate site location factor.

What Columbus and other growth markets don’t want is the rising housing costs of fast-growing markets such as Austin, Nashville, Charlotte, and elsewhere. As the table above illustrates, these booming urban markets are reaching the point of cost of housing impacting their competitiveness for corporate site location projects. Companies won’t locate in a region where their workers cannot afford housing.

Rural communities face the opposite challenge of booming urban markets. The depopulation of rural counties across the United States and the world, not only jeopardize the attraction of new companies to rural markets in search of workers but also does not attract much if any new housing development to these regions. Without new residential investment, the effort to retain rural residents is nearly impossible.

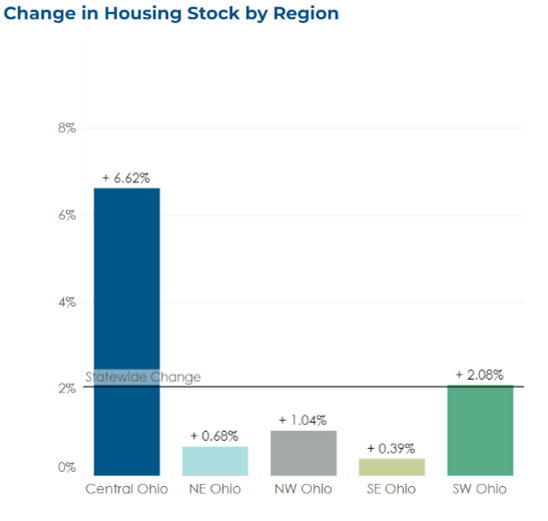

According to the Ohio Housing Finance Agency, Ohio’s housing stock has grown by 2.1% since 2010 which has outpaced population growth over the same period (+1.3%).[i] Much of this growth happened in suburban areas, while Ohio’s urban cores have seen housing stock decline (–1.4%).[ii] At the end of 2019, homeowner and rental vacancy rates–1.1% and 6.8%, respectively–were near their lowest levels on record, indicating a very tight housing market.[iii] Add in the fact that Ohio’s housing stock is relatively old, with one-in-four housing units built before 1950 (27%), Ohio communities of all sizes must get to work to attract residential builders and increase housing stock if the state wants to remain an economic development powerhouse.

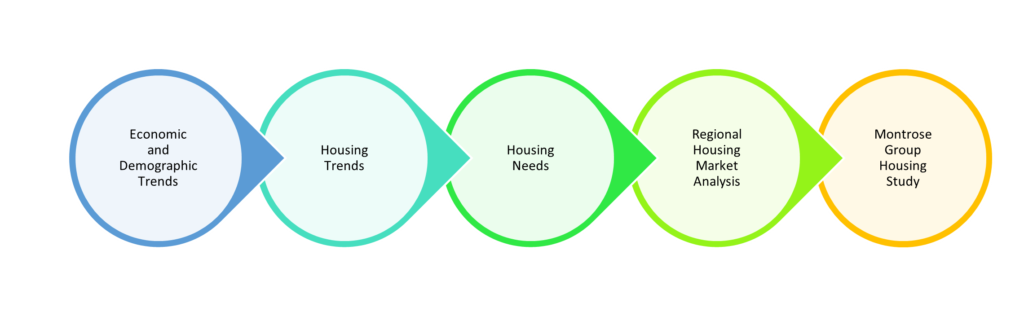

Companies and communities should begin understanding the housing a region offers through the development of a housing study.

Economic and Demographic Trends. Developing a housing study begins with research tied to regional economic and demographic trends within the community which will be the foundation for identifying the future need for diverse residential housing opportunities. Measures of economic growth, income growth, poverty, population growth, and population profile will be at the core of this analysis.

Housing Trends. Next, housing trends are examined within the region to gain an understanding of key data points that define whether the community is in a buyers-market or a sellers-market. Key data examined includes types of existing housing units within the community such as single-family and multi-family units, trends with average and median sale prices, and days on the market across multiple price points.

Forecasted Housing Needs. Next housing needs are analyzed within the region to determine the types of units needed and demanded in the market. To complete the Forecasted Housing Needs phase, an inventory of the number of occupied units versus vacant units to understand where inventory exists. Additionally, a public survey may be conducted of the community to determine the types of housing (single-family, townhomes, condos, etc.) most desirable to future buyers. This survey will look not only at the types of housing but will also examine the price bands of potential buyers, areas within the community they desire to live, and the types of floorplans (multi-story, ranch-style, etc.) most appealing to potential buyers. Employment growth over the next 10 years is measured and compared to future needs for housing units with historic trends in annual housing unit construction to determine if recent residential housing construction is meeting the needs of the market and what the estimated shortage in new home starts will be.

Housing Market Analysis. Finally, a Housing Market Analysis will be created that summarizes the current housing landscape and trends in the housing market in the community defines what potential home buyers are willing to spend on new housing and the types of housing desired by potential buyers, and identifies target areas for future residential housing growth and overlays these growth areas with forecasted housing needs of the community.

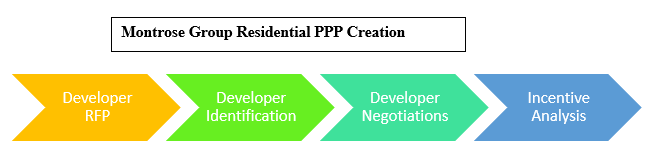

Following the development of a housing study, a local Public-Private-Partnerships PPP maybe developed to recruit a residential developer to a community. The Montrose Group supports communities seeking to develop additional residential projects through a unique approach to develop a residential Public-Private-Partnership.

Developer Request for Proposals (RFP). A local government or economic development organization to develop an RFP to solicit proposals from qualified developers to partner with the local government/EDO for the site project. Montrose ensures the RFP is formulated so that developers or development teams can bid on all or parts of the local government/EDO site development project, based on the suitability of the developer in each phase and the desire of the developer to engage in particular phases of the project. A master developer may be sought, if so desired by the developer or a series of developers will be sought for each phase of development.

Developer Identification. Next, local government/EDO officials need to identify a group of developers in the region familiar with the community and its residential market. Often a one-page project brief will be created that describes in addition to the RFP to share with potential developers to gauge their interest in the project.

Incentive Analysis. The site and the developer may require incentives in the form of tax abatement, tax increment financing or other public financing programs to make the site economically feasible for development. An economic development incentive analysis must be completed that will underscore the financial benefits of these economic development incentives and will work with the local government/EDO to determine the best path forward with regard to the economic development incentives.

Developer Negotiation. Negotiations then begin with interested developers. Developers may be required to submit an RFP that will be scored by the local government/EDO. Interviews may follow the RFP submission and the best developer should be chosen. The terms and conditions of the PPP will need to be negotiated through an economic development agreement.

In northwest Ohio, the city of Bowling Green has been part of significant economic development activity within the region which is expected to bring thousands of new jobs over the next five years. Under the leadership of the city of Bowling Green and its economic development agency (BGED), the city went directly to regional residential developers with an opportunity to construct residential housing on BGED-controlled property. BGED was interested in developing 9 parcels within the city limits, representing approximately 247 total acres of vacant agricultural land. Through this process, BGED aims to engage a development partner to work collaboratively to address the diverse residential housing needs in the City of Bowling Green, considering a mix of proposed residential uses, including single-family and townhome options. Rural, urban and suburban communities throughout the U.S. must take note of innovative residential housing projects being undertaken by major corporations in communities such as Bowling Green, Ohio to put themselves in the driver’s seat to lead the attraction of residential development and present compelling corporate site location advantages.

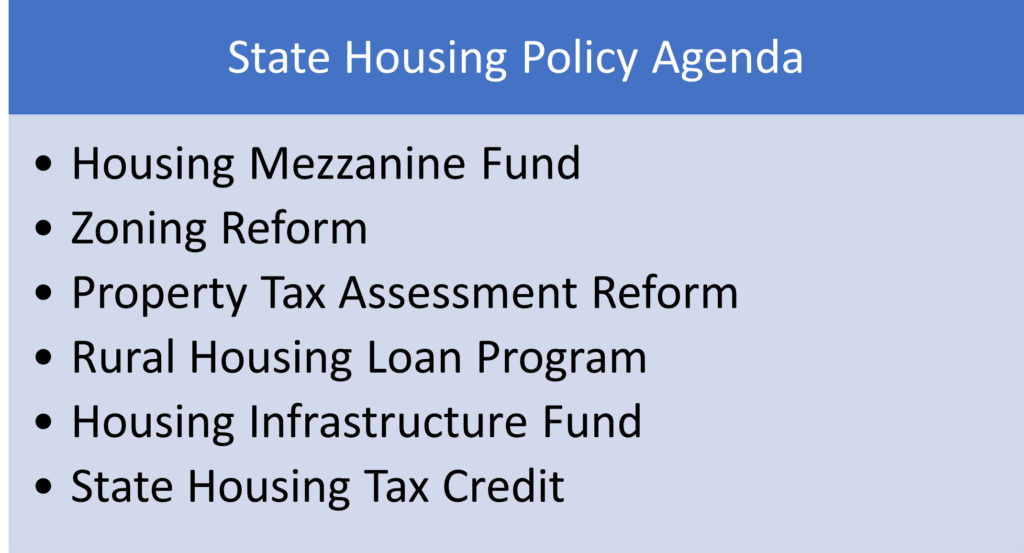

A larger solution to developing housing lies in state public policy likely resides in Statehouses across America. It is part money but part regulatory changes. Addressing the housing crisis requires state governments to launch a comprehensive policy approach focused on all housing options in urban and rural markets.

Housing Mezzanine Fund. Rising interest rates are jeopardizing major residential projects. A state housing mezzanine fund can be created from American Rescue Plan Act (ARPA) funds to match funds with lending institutions to provide mezzanine financing for residential development projects to meet the funding gap created by rising interest rates.

Regulatory Reform. A predictable land use and property tax assessment process is critical for the development of residential projects in urban and rural markets.

- Rural County Zoning. Small townships lack the ability to operate local land use programs and zoning should be in the hands of county government to ensure professional staff is in place to administer state zoning laws.

- Referendum Reform. States may only require 8% of the registered voters for a referendum on a local government ordinance or resolution to be placed on the ballot and this threshold should be substantially increased to 35% as required for the petition for a local liquor option.

- Property Tax Assessment. Again, states like Ohio operate with a complicated property tax assessment process that can impede residential institutions from predicting property tax costs. States can limit property tax appeals to only property owners, not disclose the value of the land purchase, and exempt from property tax the value of unimproved land subdivided for residential development more than the fair market value of the property for up to eight years or until construction begins or the land is sold.

Tax Abatement Reform. States should permit local governments to provide residential real property tax abatements without interference from local school districts or other taxing authorities. School districts are often the biggest opponents of residential growth even though they are in the business of serving local residents.

Rural Housing Loan Program. States should consider creating a rural housing loan program to support developers’ efforts to fund rural housing developments in rural counties.

Housing Infrastructure Fund. The availability of residential public infrastructure is essential in challenging financial markets. States can create a housing infrastructure fund from ARPA funds to award matching grants for residential public infrastructure and permit the local creation of Infrastructure Improvement Districts modeled after Transportation Improvement Districts for regional residential infrastructure efforts.

State Housing Tax Credits. The federal LIHTC program provides millions of affordable housing units. Over twenty states also created a workforce housing tax credit to provide support for LIHTC investors for their projects in the state.

The availability of housing in a market is going to be an important measure for companies considering a corporate site location project. Communities and states need to move aggressively in 2023 to address the rising housing crisis in the United States to continue to capture future job growth.